![New M4 MacBook Air On Sale for $949 [Deal]](https://www.iclarified.com/images/news/96721/96721/96721-640.jpg)

![iFixit Tears Down New M4 MacBook Air [Video]](https://www.iclarified.com/images/news/96717/96717/96717-640.jpg)

![9to5Rewards: Last chance to win a MacBook Pro from Chargeasap [Giveaway]](https://i0.wp.com/9to5mac.com/wp-content/uploads/sites/6/2024/10/M4-MacBook-Pro-doesnt-tempt-me-because-Apple-Silicon-Macs-are-almost-too-good.jpg?resize=1200%2C628&quality=82&strip=all&ssl=1)

![[The AI Show Episode 139]: The Government Knows AGI Is Coming, Superintelligence Strategy, OpenAI’s $20,000 Per Month Agents & Top 100 Gen AI Apps](https://www.marketingaiinstitute.com/hubfs/ep%20139%20cover-2.png)

![[The AI Show Episode 138]: Introducing GPT-4.5, Claude 3.7 Sonnet, Alexa+, Deep Research Now in ChatGPT Plus & How AI Is Disrupting Writing](https://www.marketingaiinstitute.com/hubfs/ep%20138%20cover.png)

![How to become a self-taught developer while supporting a family [Podcast #164]](https://cdn.hashnode.com/res/hashnode/image/upload/v1741989957776/7e938ad4-f691-4c9e-8c6b-dc26da7767e1.png?#)

.jpg?width=1920&height=1920&fit=bounds&quality=80&format=jpg&auto=webp#)

.jpg?#)

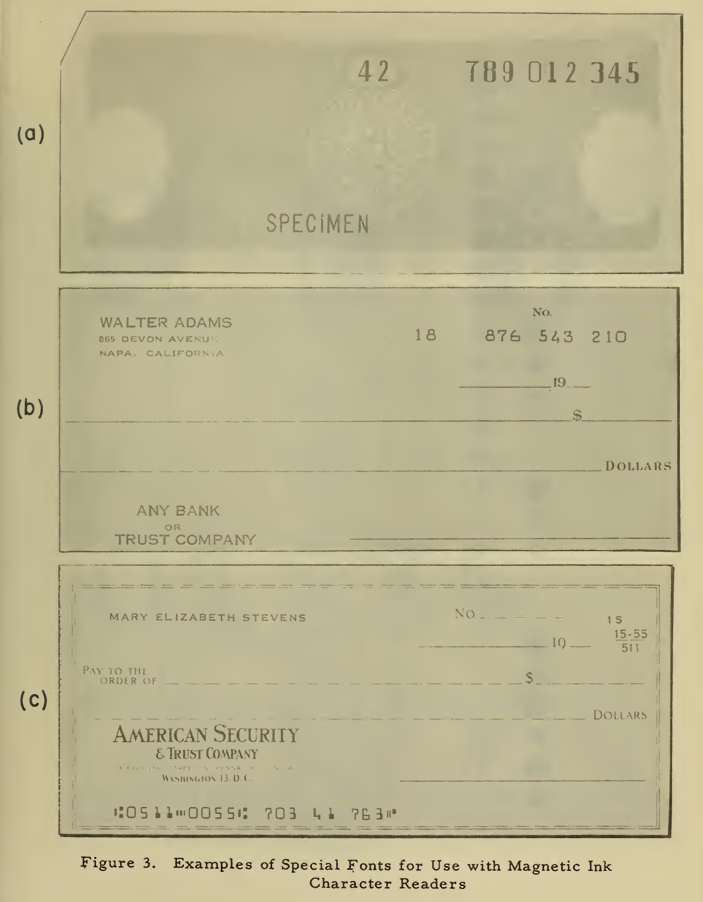

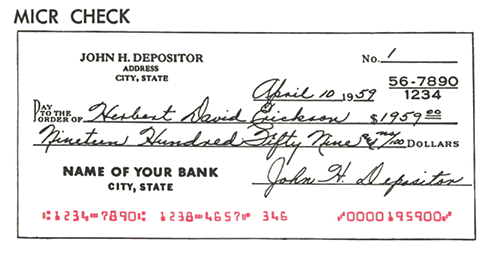

How Magnetic Fonts Twisted Up Numbers And Saved Banking Forever

If you’ve ever looked at the bottom of a bank check, you probably glanced over some strangely formed numbers? If you’re a fan of science fiction or retro computers, you’ve …read more

If you’ve ever looked at the bottom of a bank check, you probably glanced over some strangely formed numbers? If you’re a fan of science fiction or retro computers, you’ve probably spotted the same figures on any number of books from the 1980s. They’re mostly readable, but they’re chunky and thin in places you don’t expect.

Those oddball numerals didn’t come from just anywhere—they were a very carefully crafted invention to speed processing in the banking system. These special fonts were created to be readable both by humans and machines—us with our eyes, and the computers with magnetic sensors. Let’s explore the enigmatic characters built for Magnetic Ink Character Recognition (MICR).

Machines Will Do The Work

These days, much of the money in the world is sent and received via digital transfers. Once upon a time, though, paper was king when it came to moving money. The almighty check was how you got money out of one account and into another one.

Sadly, as populations grew and economic activity skyrocketed, the status quo couldn’t hold. By the mid-1940s, the problem was already apparent, with the Federal Reserve dealing with 2 billion checks a year in 1946. While mechanical adding machines and various other techniques helped, fundamentally, bankers and clerks were processing millions of checks daily, all by hand.

The financial world needed a way to speed handling of checks as much as possible. The solution was to enable machines to read as much of the information on a check as possible, so they could handle the basic sorting and processing steps at speed. This would eliminate much of the manual reading and handling by humans, and greatly improve throughput.

The problem was that in the middle of the 20th century, technologies like optical character recognition, or even digital cameras, were decades away. Instead, the key innovation that saved banking was MICR—short for Magnetic Ink Character Recognition. It involved printing certain characters on checks with an iron oxide-based ink. The combination of the ink’s magnetic content and the unique shape of each number meant machines could read the checks easily and unambiguously—even in the case they were physically damaged. Meanwhile, the MICR characters were also designed to remain human readable, so they could be readily understood by the humans using them, too. This was an important backup in the event a check failed machine reading for whatever reason.

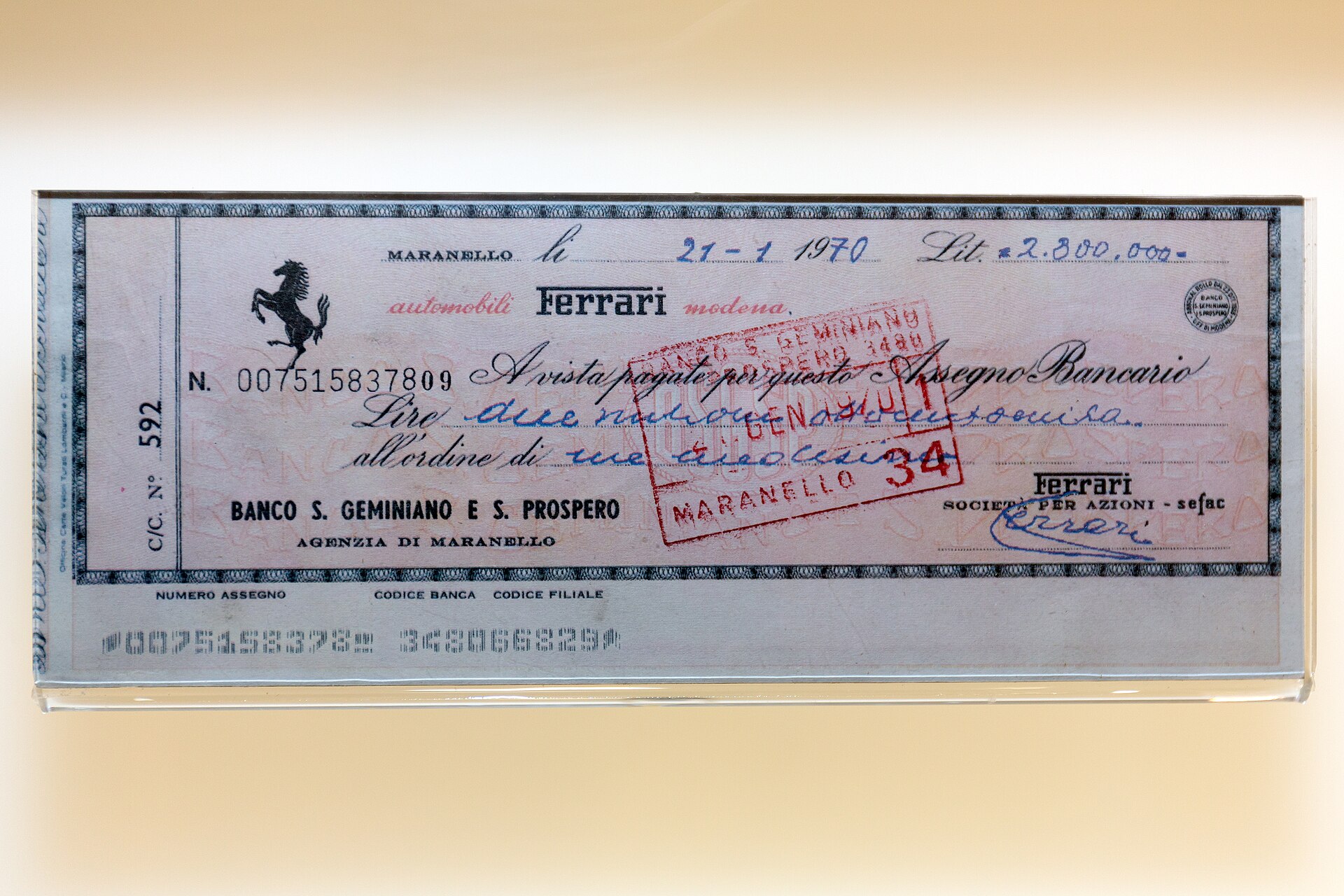

With MICR, checks could be pre-printed with a bank’s routing number and the customer account to draw from, leaving just the payment amount to be read from the check user’s handwriting. Alternatively, even the amount could be printed in MICR characters if the check was fully machine-issued, speeding processing further. With the aid of magnetic ink, processing speeds went up prodigiously. In 1950, mechanical aids had allowed one clerk to process 1,300 checks in an hour. Fast forward to the magnetic ink era just a few years later, and clerks were able to handle 33,000 checks or more in the same amount of time.

As is so often the way, the world did not agree on one standard for MICR purposes. Developments across the banking world occurred during the 1950s, with two major magnetic fonts being developed in parallel.

If you’re based in the United States, Canada, the UK, Australia, or much of the rest of the English-speaking world, you’re probably most familiar with a font called E-13B. This is the one with the gloopy letters and the worst ‘1’ numeral ever committed to print. It was developed by General Electric and the Stanford Research Institute. Its designation was entirely pragmatic—E denoted that it was the fifth font considered, and B denoted the second revision. 13 referred to the fact it was designed for use on an 0013-inch grid.

The font was designed to create a unique magnetic signal pattern when each numeral or symbol was scanned by a magnetic reader. The shapes were specifically engineered to avoid any possible confusion – that’s why the 0 has those straight sides, and the 8 is so hefty at the bottom, for example. Each number generates a waveform that’s distinct from the others, making it easy to process the signal and read the check accurately. E-13B wasn’t perfect, with 2s and 5s putting out rather similar signals in some cases that could cause confusion, but it proved itself more than reliable enough to do the job.

The standard was trialled in 1956 and was adopted by the American Bankers Association by 1958. By 1963, the American National Standards Institute (ANSI) designated that E-13B would be the standard, and by 1967, the Federal Reserve mandated the use of magnetic ink on checks. E-13B went on to become a graphical motif commonly associated with computers and modernity, with artists commonly creating lookalike characters for the whole Latin alphabet. However, the official E-13B standard only ever had 14 characters—numerals 0 to 9, plus four additional control characters for check processing—”transit,” “on-us,” “amount,” and “dash.”

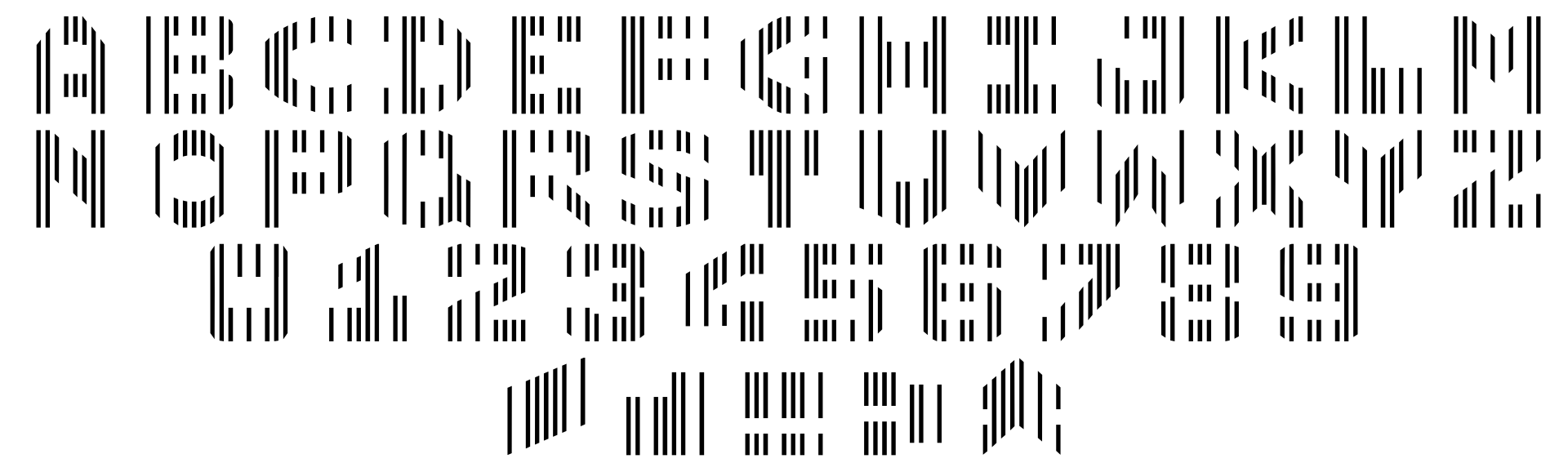

At roughly the same time, French computer company Groupe Bull was working on its own standard. In 1957, it developed the CMC-7 font, which used an entirely different approach to E-13B. Rather than relying on the varying the intensity of magnetism by the amount of ink in a character, CMC-7 instead relied on characters made up of vertical bars. The spacing between the bars could be read by machine to determine the numerals. The design gave CMC-7 characters more of a barcode-like appearance. Notably, CMC-7 also featured a full alphanumerical character set—41 glyphs, including A-Z, 0-9, and five control characters.

Thanks to the geopolitics of the mid-20th century, each MICR standard ended up with its own stomping ground. While E-13B dominated in the Anglophone world, CMC-7 ended up being used in France, Spain, and much of Europe and South America. At heart, both standards did the same thing—they enabled machines to read most of the data on a check with a minimum of fuss.

Banks might feel mostly digital these days, but MICR fonts are still an important standard in the financial world. If you’re issuing checks, you might end up running into some problems if you’re not printing them with the appropriate MICR font and magnetic ink. For most of us, checks are a simple tool of the past, but it turns out a great deal of engineering went into perfecting them before the computer came along.